Electronic payments have become the standard for many businesses across industries. Customers increasingly prefer to pay using credit cards, debit cards, and digital wallets because these methods are fast and convenient. While card payments improve the customer experience and help businesses increase sales, they also introduce processing fees that can...

Payments for Nonprofits & Churches: Recurring Giving, Text-to-Donate, and Compliant Donor Receipts

Nonprofits and churches increasingly rely on digital payment tools to support their missions. In today’s world, it has become essential for nonprofit organizations to offer donors ease, flexibility, and transparency in making donations to their favorite causes. In other words, digital payment options have become integral to nonprofit organization operations in...

Interchange Fees Explained: How They Impact Small Business Profit Margins

For many small business owners, credit card payments are a necessity rather than a choice. Customers expect to swipe, dip, or tap their cards without hesitation. While card acceptance boosts sales, it also introduces costs that can quietly shrink profits. One of the most significant of these expenses is interchange...

Practical Strategies to Reduce Credit Card Fees Without Switching Providers

For many businesses, credit card payments are essential to daily operations. Customers expect the convenience of swiping or tapping their cards, whether shopping online or in person. However, processing those transactions comes with costs that can slowly eat into profit margins. Many merchants believe that the only way to reduce...

Breaking Down Credit Card Processing Fees: What Small Businesses Are Really Paying

For most small businesses today, accepting card payments is not optional. Customers expect to pay with debit cards, credit cards, mobile wallets, and contactless tap systems. While this convenience helps drive sales, it also comes at a cost. Many business owners see deductions from their daily sales deposits but do...

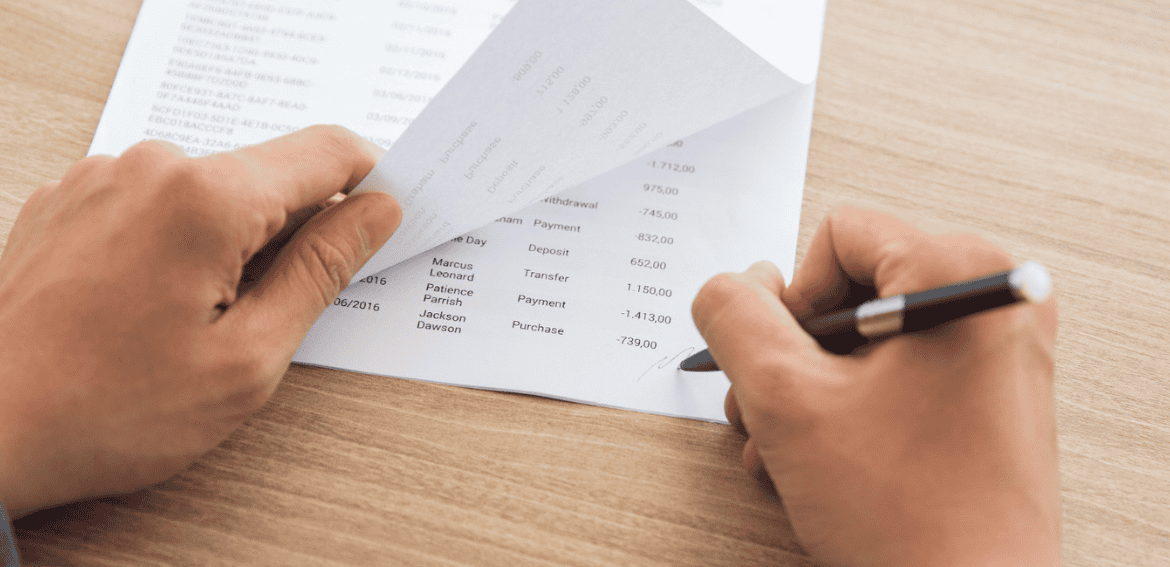

Payment Reconciliation: How Merchants Match Batches Deposits and Statements

For many merchants, accepting payments feels straightforward on the surface. A customer pays, the transaction is approved, and funds appear in the bank account days later. Behind the scenes, however, payment processing is made up of multiple moving parts that do not always line up neatly. Card batches, processor deposits,...

How Acquirers, Issuers, and Card Networks Connect the Payment Ecosystem

Every time a customer taps a card, shops online, or pays through a mobile wallet, a complex process runs quietly in the background. Money does not move directly from a customer’s bank account to a merchant’s account in a simple step. Instead, several specialised institutions work together to approve the...

Card Present Payments vs Card Not Present Payments: How Processing Changes

The way people pay for goods and services has changed dramatically over the past two decades. Customers now move easily between shopping in physical stores, ordering online, paying through apps, and completing transactions over the phone. For businesses, this shift has introduced different payment environments that operate under separate rules....

Authorization, Clearing, and Settlement: The Three Stages of a Card Transaction

Every time someone taps a card at a store, enters details online, or pays through a mobile wallet, a complex financial process unfolds in the background. To the customer, the payment feels instant. To the merchant, it appears straightforward. Yet behind the scenes, multiple financial institutions and systems work together...

Breaking Down Interchange Fees, Assessments Fees, and Processor Fees

Payment processing fees are one of the most common sources of confusion for business owners. Many merchants see deductions on their statements without fully understanding where those costs come from or why they vary from one transaction to another. While fees may look complicated at first glance, they are built...